The financial performance of supermarkets during the second half of 2012 is looking just a little bit better than the first half, industry analysts told SN.

A slowdown in inflation, combined with a slow but ongoing acceleration in the general economy, should produce second-half results that are “a smidge better than they’ve been,” Scott Mushkin (right), managing director for Jefferies & Co., New York, said. “The second half won’t be great, but it looks like it will be a bit easier for most companies.”

A slowdown in inflation, combined with a slow but ongoing acceleration in the general economy, should produce second-half results that are “a smidge better than they’ve been,” Scott Mushkin (right), managing director for Jefferies & Co., New York, said. “The second half won’t be great, but it looks like it will be a bit easier for most companies.”

Andrew Wolf, managing director for BB&T Capital Markets, Richmond, Va., also said he expects supermarkets to see modest volume gains in the second half “as the U.S. economy slowly improves and as long as food inflation doesn’t ramp up — though results could still be negatively affected by the fiscal crisis in the U.S. and the debt crisis in Europe.”

While food producers will face increasing costs due to the drought and herd liquidations, Wolf said he expects them to absorb those costs through the balance of 2012 before beginning to pass them through in the first half of next year.

Bryan Hunt, managing director for Wells Fargo Securities, Charlotte, said sales comparisons should be easier in the second half “because the very mild weather at the end of 2011 resulted in a lot of meals away from home, and a shift to more meals at home this year should produce better results.”

Raw material costs were volatile in the second half of 2011, Hunt added, “resulting in a lot of price calisthenics for supermarkets to be able to manage their costs. But less inflation to pass on to consumers during the second half of this year should contribute to better value propositions for conventional supermarkets.

“In addition, there was a pantry de-stocking in 2011 that led to weak Center Store sales, while more recent sales trends have flattened out, which implies a potential end to the de-stocking phenomenon.”

Click on the image for a larger version.

Chuck Cerankosky, managing director for Northcoast Research, Cleveland, was a bit more pessimistic than his peers, telling SN he does not expect much change in the industry in the second half, compared with the first. “There will be incremental improvements as the economy grows and employment numbers go up, but it will happen a bit at a time. Nothing will change for the better very quickly.”

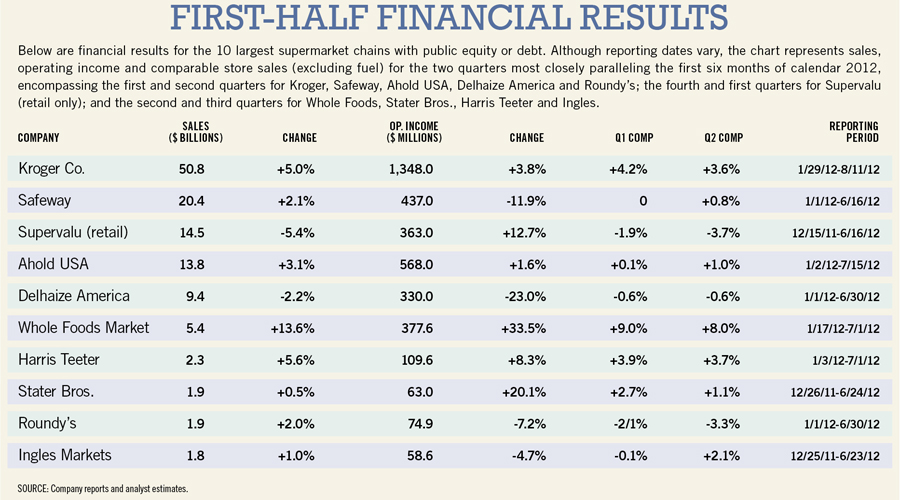

The financial performance for the top 10 publicly held chains during the first half of 2012 were mixed, compared with their performance in the first half of 2011:

• Sales for the group were 3.5% better in this year’s first half.

• Operating income increased 1.2% in the half.

• Comparable-store sales were lower in the first half of 2012, rising an average of 1.5% in the first quarter of the calendar year, compared with an average increase of 1.8% in the prior year’s period; and increasing an average of 1.3% for the second quarter, compared with an average increase of 2.6% a year earlier.

Excluding the results at Whole Foods Market — which far outpaced any other operators — comps were up an average of just 0.7% in the first quarter of 2012, compared with 1.2% a year earlier; and up an average of 0.5% in the second quarter this year, vs. a 2% increase in last year’s second quarter.

According to Wolf (right) , inflation for the first half of this year was running at about 3.3%, “so virtually all the sales growth came from retail inflation. Sales were generally just a little stronger than the underlying inflation, with first-quarter volume flat to down and second-quarter volume flat to up.

According to Wolf (right) , inflation for the first half of this year was running at about 3.3%, “so virtually all the sales growth came from retail inflation. Sales were generally just a little stronger than the underlying inflation, with first-quarter volume flat to down and second-quarter volume flat to up.

“As a result, the stronger conventional players generally saw a little bit of improvement in volume trends as inflation dropped from 3.8% in the first quarter to 2.7% in the second — and while comparable store sales were still down in real terms, they were down less as volume improved.”

Read more: Bleak Expectations: Financial Pressures Worry Analysts

Wolf said food deflation drove strong first-half sales in the produce department, “which had a positive impact on overall tonnage, and as a result actual sales looked better than what was reflected in the Nielsen and [Symphony]IRI numbers,” Wolf added.

“Although inflation was a positive factor and had some impact during the half,” said Mushkin, “customers really weren’t seeing any improvement in their economic situations, meaning that whatever supermarkets gained on inflation, they lost on the negative reaction to higher prices.”

Most of the sales improvements during the half were driven primarily by inflation, he noted, “and the industry continued to struggle as middle-class shoppers had to deal with rapidly rising prices for everyday items like food, and employment levels were not great.”

Read more: Analysts Ponder: Is Kroger All It Can Be?

Cerankosky said the industry continued to face “a challenging sales situation” during the first half, with consumers remaining cautious and unwilling to trade up while the economic recovery remained slow and unemployment stayed high. “As a result consumers generally reduced discretionary purchases in their food budgets — often choosing to cut back on groceries to use the money for other purposes.”

Hunt said supermarkets were negatively impacted at the end of 2011 by “a lot of sales and earnings disappointments” that carried over into the first half of 2012.

Here are each chain’s results for the quarters most closely paralleling the first half of the calendar year:

Kroger, Safeway, Supervalu

• KROGER CO., Cincinnati, saw sales jump 5% to $50.8 billion during the first half; operating income was up 3.8% to $1.4 billion; and identical sales rose 4.2% in the first quarter and 3.6% in the second.

Kroger continued to distance itself from its publicly held conventional competitors during the half, Mushkin said, “and the results were good — not quite outstanding but really solid, considering the environment. While most of the industry found itself struggling during the half, Kroger didn’t because it had better pricing and better execution.

“Unlike some other chains, Kroger did not see a lot of mass-merchandiser openings against it during the half, and that, combined with good pricing and great service, enabled it to differentiate itself. And it was able to achieve share gains without sacrificing too much margin.”

Cerankosky said Kroger also benefited from “a top-notch private-label program” and from offering customers cash rewards, “which continued to be very popular during the half.”

According to Wolf, Kroger continued to rely on its sales productivity model — reinvesting gross profits into price to drive traffic — “and that continued to work because the company has been willing to combine its own supermarket mindset with the economic overview from Dunnhumby to develop more efficient promotions.”

Kroger also drove labor productivity with a new front-end program it introduced during the second quarter in which it opens more checkstands as needed to reduce customer checkout times — “a productive model that doesn’t require adding staff,” Wolf noted.

Read more: Analysts Ponder: Is Kroger All It Can Be?

• SAFEWAY, Pleasanton, Calif., experienced a sales increase of 2.1% to $20.4 billion for the half; a drop in operating income of 11.9% to $437 million; and flat identical-store sales in the first quarter and an increase of 0.8% in the second.

Safeway is still making “slow progress toward a nice sales recovery,” Cerankosky said, “and that’s limiting the growth of its operating income as it invests in price and the up-front costs of Just for U” — the digital program that went chainwide during the half.

According to Wolf, Just for U enabled Safeway to make sales gains “at the same time it has continued to put more gross margin into driving sales.”

Like the Kroger model, Just for U allows Safeway to have more efficient promotions because it offers price savings to consumers who are already in its stores, Wolf explained, “and getting them to buy just one extra item helps pay for the program.”

Safeway showed very gradual improvements in sales productivity during the half, he added, “so although ID sales remained weak, they were less weak.”

For Mushkin, the turnaround at Safeway “is taking longer than expected. Programs, like Just for U are gaining some traction, but the company is still being overwhelmed by the tough economy and by competition, particularly the aggressive opening of Wal-Mart formats in its marketing areas, which will mean an uphill battle for Safeway.”

• SUPERVALU, Minneapolis, whose retail operations experienced a sales decline of 5.4% to $14.5 billion for the half; a rise in operating profit, excluding impairment charges, of 12.7% to $363 million; and comp sales of negative 1.9% in the company’s fourth quarter and negative 3.7% in its first quarter.

Supervalu’s retail banners were under “significant pressure” during the first half of the calendar year, Hunt indicated, with traffic declining in the mid-single-digit range because of prices that were approximately 10% higher than the rest of the market.

However, the company did reduce the pricing gap on produce during its fourth quarter and on Center Store merchandise during its first, “and it got sharper on private-label pricing,” Hunt pointed out.

According to Mushkin, what’s ironic about the positioning of Supervalu’s chain business is “that prices were less out of line during the first half than they’ve been in five years, though they’re still not where they need to be. But the business continued to struggle as the banners continued to lose relevance in their markets.”

Cerankosky said Supervalu’s results represent “the ultimate sales shortfall,” with approximately 18 consecutive quarters of negative comparable-store sales, “and those results have affected its operating expense structure, resulting in disappointing earnings.”

Although the company saw some earnings improvement in its fourth quarter, the numbers were disappointing in the succeeding quarter, “because sales were not sustainable enough to bring the improvements down to the bottom line,” Cerankosky added.

According to Wolf, Supervalu was hurt by its heavy overlap with both Safeway and Wal-Mart Stores. “Wal-Mart’s current pricing strategy [involving customer testimonials comparing its prices with those of conventional chains in different markets] is designed to embarrass other retailers, and the higher prices at the Supervalu banners made them an easy target — at the same time Safeway’s Just for U also had a negative impact on those stores.”

Ahold USA, Delhaize America, Whole Foods

• AHOLD USA, Quincy, Mass., reported a sales increase of 3.1% to $13.8 billion for the half; an increase in operating profits of 1.6% to $568 million; and ID sales up 0.1% in the first quarter and 1% in the second.

Edouard Aubin, a Paris-based analyst with Morgan Stanley, New York, said Ahold, which operates the Stop & Shop, Giant-Landover and Giant-Carlisle banners in the U.S., continued to exhibit “significant price gaps” with its competitors, with average baskets, including promotions, running 10% to 15% above Wal-Mart.

Ahold’s price positioning “seems to be uncompetitive overall,” he added, though volumes have held up, despite competing against “some of the weakest players in the U.S.,” including A&P and Shaw’s, he noted.

Aubin also said Ahold’s comp volumes have been close to flat for the past three years, which could lead to further margin erosion.

• DELHAIZE AMERICA, Salisbury, N.C., saw sales decline 2.2% to $9.4 billion in the half; operating income drop 23% to $330 million; and comparable-store sales fall 0.6% in both the first and second quarters.

The declines in results are due to Food Lion’s struggles to fend off Wal-Mart in several markets, Wolf said. Although Food Lion is trying to improve its pricing in some markets, “it still remains out of line in others,” he added, and Wal-Mart’s advertising campaign has been “particularly effective against Food Lion in most areas.”

Aubin said remodeling activity by Food Lion — 172 stores in May 2011, followed by 268 more by last March — is paying off, with volume growth 8% to 10% above the rest of the chain at those stores. However, despite “meaningful price investments” in the remodeled stores, “it seems the company has continued to protect its cash-flow generation at the expense of the top line,” Aubin noted.

According to Mushkin, Food Lion has been trying to get its prices more in line, “but it’s been struggling mightily because its bread-and-butter demographic is people in the first, second and third quintiles — from the poorest to those at the low- to middle-income levels — that are under the most pressure, and that’s the same group Wal-Mart goes after.

“Food Lion’s prices tended to be about 15% higher than Wal-Mart’s during the half, but with inflation, that’s a very substantial amount for a family of four, and if that family feels it can save $40 or $50 a week at Wal-Mart, that creates a fundamental problem for Food Lion.”

Hannaford is better positioned than Food Lion, Mushkin added, because, although its pricing is similar to Food Lion’s, it meets the needs of middle- to upper-middle-class customers in the Northeast. Sweetbay represents only a small part of Delhaize’s U.S. business, he pointed out.

• WHOLE FOODS MARKET, Austin, Texas, experienced a sales jump of 13.6% to $5.4 billion during the first half; an increase in operating profits of 33.5% to $377.6 million; and ID sales that rose 9% in the company’s second quarter and 8% in its third.

Whole Foods’ comps “continued to be incredible” in the first half due to better shrink control, labor systems, cost containment and productivity enhancements, Mushkin said. “A lot of what Whole Foods is doing is as simple as where it places merchandise, but it’s all clearly helping boost margins,” he said.

According to Wolf, “Whole Foods is continuing to execute terrifically well, bringing down store labor to gain operating leverage and succeeding at creating a better value image — at the same time it’s continuing to bring new customers into its already busy stores. And it’s ramping up its new-store growth into what it considers smaller markets, though most of those are more midsize markets at least,” he said.

Cerankosky said Whole Foods’ stores are well distributed geographically, “and it carries a product mix that’s very differentiated and that resonates with consumers who are looking for high quality and who lean toward natural and organic foods.

“It also offers a format that attracts consumers with higher incomes, which means customers are buying additional items and trading up when they shop.”

Harris Teeter, Stater Bros., Roundy's, Ingles

• HARRIS TEETER, Matthews, N.C., experienced a 5.6% sales increase to $2.3 billion; a rise in operating profits of 8.3% to $109.6 million; and comp increases of 3.9% in its second quarter and 3.7% in its third.

Harris Teeter continued to benefit from operating differentiated stores, Wolf pointed out — “stores that remain conventional but are closer than any other public conventional chain to Whole Foods in terms of quality and merchandising, though with slightly sharper price points.”

The chain invested in pricing during 2011 “to promote a better value equation in the post-recession period,” Wolf added, “but it was able to take its foot off the accelerator during the first half as demand went up.”

According to Cerankosky, Harris Teeter is “very well run and very well positioned. While it’s different than Whole Foods, it’s been able to carve out a quality niche in its marketing area versus competing supermarkets, just as Whole Foods has done.

“The stores offer high service levels, good quality foods, a strong private-label program and price points on ad features that enable it to compare favorably with Wal-Mart because it selects the items it wants to compare rather than letting Wal-Mart choose the items it wants to compare.”

• STATER BROS. MARKETS, San Bernardino, Calif., reported a sales increase of 0.5% to $1.9 billion for the half; an operating profit increase of 20.1% to $63 million; and comp increases of 2.7% in its second quarter and 1.1% in its third.

Hunt said Stater’s second-quarter comps were stronger than most of the chain’s peer group because sales were strong, reflecting sharp pricing and an advertising program carried over from the company’s first quarter that promised, “Always get more for less,” “which resonated well with customers in the Inland Empire of Southern California.”

The company also benefited from good forward buys, he said, “which is one reason earnings expanded nicely. And while gross margin was generally under pressure across the industry, margins at Stater rose 100 basis points during its second quarter.”

• ROUNDY’S MARKETS, Milwaukee, had first-half sales rise 2% to $1.9 billion; operating profit fall 7.2% to $74.9 million, excluding extinguishment of debt; and ID sales of negative 2.1% in the first quarter and negative 3.3% in the second.

Conversions of several Wal-Mart discount stores to supercenters in Roundy’s two major markets, Milwaukee and Minneapolis, along with the addition of Pfresh sections at several Target stores hurt Roundy’s during the half, Wolf said.

According to Mushkin, “Roundy’s is a well-run company with a strong market position, but it’s dealing with a large number of supercenter openings that don’t look like they will abate, and that’s creating havoc as Roundy’s tries to get pricing more in line.”

The chain began introducing an everyday pricing program late in the first half, “but its stores tend to appeal to a middle-class demographic that’s under enormous amounts of economic pressure, and though those consumers might like Roundy’s service and perishables, they’re going for price, and our surveys show a basket of goods at Roundy’s is priced about 20% above Wal-Mart,” Mushkin said.

Read more: Bleak Expectations: Financial Pressures Worry Analysts

• INGLES MARKETS, Asheville, N.C., saw sales up 1% to $1.8 billion for the half; operating profits fall 4.7% to $58.6 million; and a decline in comps of 0.1% in the second quarter and an increase of 2.1% in the third.

Hunt said the poor comps in the company’s second quarter reflected the warm weather in Ingles’ marketing area early in 2012, which limited sales of seasonal general merchandise and also prompted more meals away from home — in contrast to one of the coldest winters early in 2011, which made comparisons tougher than usual and hurt operating margins for the half.

Results at Ingles were more normalized in the company’s third quarter, he pointed out, “and the chain also benefited from very good fuel margins, along with more normal temperatures and easier comparisons, with gross margins up 10 basis points.”

| Suggested Categories | More from Supermarketnews |

|

|

|

|