Retailers are considerably more optimistic about their prospects for the year ahead than they were early last year, according to a survey conducted by SN.

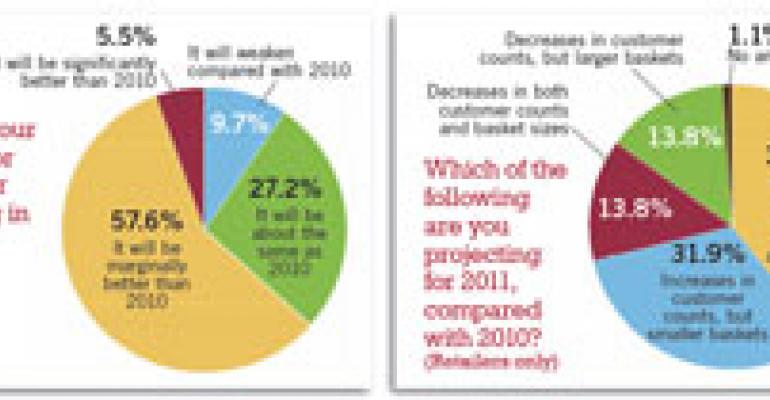

While more than half of all retailers polled early in 2010 said they expected last year to be about flat or worse than in 2009, retailers polled this year were much more upbeat — 62.8% of retailers said they expected consumer spending to be at least marginally better, with nearly 10% saying they expect spending to be “significantly” better than last year.

Of the total respondents, which also included manufacturers and others, such as brokers and wholesalers, 57.6% said they expected consumer spending to be “marginally” better than last year, and 5.5% of the total said they expected spending to be “significantly” better.

The survey was conducted online among subscribers to SN's daily email newsletter Feb. 18 to March 1.

Despite concerns among analysts about retailers' ability to pass on cost inflation, however, retailers seemed to feel they would be able to do so. Retailers projected shelf-price increases on par with increases on the cost side, and also said they expected profitability to improve in 2011.

None of the 217 poll respondents (including 94 retailers) said they expected deflation in 2011. Most retailers (60.6%) said they are expecting their food costs to rise between 2.1% and 5% this year, and the same proportion said they expect shelf prices to rise at the same level.

Almost 10% of respondents — 9.6% — said they expect their food costs to increase by more than 5% in 2011, and again the same percentage of retailers expect shelf prices to increase by the same amount.

In recent conference calls discussing financial results, many retailers said they had indeed been successful so far in passing along price increases to consumers, and were cautiously optimistic about being able to do so.

Steve Burd, chairman, president and chief executive officer, Safeway, Pleasanton, Calif., recently said inflation at the retail shelf was “running in the 0.5% to 0.7% range” in the first quarter.

“But we continue to see inflation in cost of goods,” he added. “We pass those along to consumers. As we observe other retailers — and I would include price formats, you name it — we monitor their price increases, and I would tell you that it's our observation that virtually all retailers are passing it along.”

Burd noted that some regions are “stickier” than others in terms of retailers' reluctance to pass along price increases, but overall there has been “no real difficulty” in raising shelf prices lately.

He suggested that the current inflationary trend is in its early stages, and that retail shelf prices overall could go up 2% or more.

Brian Todd, president and CEO, The Food Institute, Upper Saddle River, N.J., pointed out that the difference between the Producer Price Index and the Consumer Price Index has been narrowing, indicating that food retailers are indeed starting to raise shelf prices after holding back on increases throughout much of 2010.

“They have done an excellent job of [passing along price increases] so far, but it poses challenges in the future, especially in the center of plate items — beef, pork, poultry — it's a little more difficult to control those.”

The recent rise in fuel prices could eventually work their way into product costs, and a steep increase in transportation costs might accelerate inflation, he pointed out, but overall suppliers can mitigate some fuel-cost increases with cost cuts in other areas, such as marketing, promotions and labor.

The food-at-home portion of the CPI rose 2.1% for the 12-month period through January, the U.S. Department of Labor reported, marking a relatively sharp increase at year-end as retailers began to recover from a period of deflation and intensified promotional activity on the part of competitors.

Burd of Safeway said irrational pricing by other food retailers has largely abated, even for items with volatile pricing such as milk and other perishable commodities.

“Today, if we get a 15-cent a gallon increase in milk, the retail goes up 15 cents,” he said, explaining that competitive pressures during the recent recession might have prevented such shelf-price increases.

Cincinnati-based Kroger Co. said it experienced cost inflation of about 2.3% in the fourth quarter, excluding fuel, and that it, too, has been able to pass along these increases at the shelf. Much of that inflation was driven by meat-cost increases, although grocery departments were up 1%.

“This follows six consecutive quarters of deflation in the grocery department,” said Rodney McMullen, president and chief operating officer, in a conference call discussing fourth-quarter financial results. “We are passing along product cost increases from national-brand suppliers in grocery today, and we plan to continue to do so.”

David Dillon, chairman and CEO, said he was “pleased” with the reversal of grocery deflation, and added that he was “bullish” on Kroger's prospects for the current year, citing gains in both tonnage and price.

In SN's economic outlook survey, more than half of retailers (57.4%) said they expected most or all of their sales gains in 2011 to come from inflation.

Slightly more than half of retailer respondents said they expected larger basket sizes in 2011, and significantly more than half (71.3%) said they expect increases in customer counts. Only 13.8% said they expect decreases in both customer counts and basket sizes.

In the 2010 version of the survey, retailers were much more skeptical of their ability to grow the size of their average shopping trip, with just over 70% predicting smaller baskets.

Interestingly, retailers' increase in optimism comes against a backdrop of anticipated increases in competitive pressures.

More than 95% of retailers in the survey said they expected competitive pressures to be about the same or increase, with 28.7% saying they expected competitive pressures to increase significantly and 35.1% saying they expected a slight increase in competitive pressure. Only 3.2% said they expected a decrease in competitive pressures during 2011.

Also, retailers said they expected to engage in more price-focused advertising this year than last, with more than half (52.1%) saying price-focused advertising would be up “a little,” and 16% saying it would be up “a lot,” compared with 2010.

Although private-label growth has slowed from a spike in 2009, more than 85% of the retailers in the survey said they expect dollar sales of private label to grow as a percent of overall sales in 2011. The proportion expecting private-label label growth is similar to results from the survey a year ago, when 86.3% said they expected dollar-share growth among private brands.

Jon Hauptman, partner in consulting firm Willard Bishop LLC, Barrington, Ill., said he expects retailers will continue to expand their private-label offerings — particularly those at the lowest-price-point tier, in the midst of growing food inflation.

The emphasis on store brands provides “a way for shoppers to continue to shop the store and provide even more opportunities to save,” he explained.

“The continued focus on store brands will be on not only highlighting store brands throughout the store through merchandising, but also through promotion.”

Retailers will likely work more diligently to highlight the availability of these private-label items, he said.

In addition, supermarket operators can be expected to hone their pricing and value messages even further in an inflationary environment, with an opportunity to optimize endcap promotions.

“We'll also see more retailers refocus defining what value means in their stores and defining how a shopper can save in their store.”

Hauptman said he agrees with the retailer optimism expressed in the survey. “Many retailers will thrive in this environment. Those that will be successful will be those that do a good job of communicating how shoppers can save in their stores, even in light of increasing prices.”

Some Skeptics

Despite retailers' confidence, some analysts remain skeptical that all supermarket operators will be able to pass on their cost increases and enjoy improved results in 2011, especially given the increasing emphasis on food in nontraditional formats and the ongoing growth of Wal-Mart and other discounters, such as Aldi and Save-A-Lot.

“We remain cautious on the food retailers given the uncertainty over whether the supermarkets will be able to pass along inflation to consumers,” Deborah Weinswig, an analyst for Citigroup, wrote in a recent report. “In addition, we expect Wal-Mart to apply even greater pricing pressure by leveraging its global scale to increase its direct sourcing penetration [currently 30%], which will allow the company to offset rising food costs and keep retail prices flat.”

She cited Supervalu, Minneapolis, as likely to be the “most negatively impacted” of the traditional supermarkets she follows, citing the company's weak price perception among consumers relative to other supermarket operators.

In a conference call with investors in January, Craig Herkert, Supervalu's chairman and CEO, conceded the company faces a difficult task in improving its price image while costs are increasing.

“We recognize the challenges inherent in making targeted price investments during a period of rising inflation,” he said. “These efforts will take time, but we have begun to take deliberate actions to implement new programs, methodically change the way we conduct business and improve price and value perception in those markets where we have been out of line.”

Herkert described his strategy for improving price perception in terms of reducing the everyday price of many items so that the gap when they are put on sale is not as great.

“What we're working on is getting away from aggressively high/low,” he said. “We are still in our traditional retail banners — most of them — a high/low retailer, and we will remain a promotional retailer. What we're trying to do is to minimize that delta we have between our regular price, which I think we referred to as ‘insult pricing’ in some cases. Get that regular price back in line with where consumers expect it to be, and yet still be a promotional merchant.”

Keith Jelinek, director in the global retail practice at consulting firm AlixPartners, said he believes supermarket operators will have a difficult time passing inflation on at the shelf, and will continue to look at other ways to cut costs to maintain margins.

“For the past year, we have been watching these rising costs coming at us, and many retailers are just hearing now about increases from manufacturers because of the increases in commodity costs,” he told SN. “We don't believe they are going to be able to pass them all on to the consumer, so we are advising them to look at other costs to reduce.”

Jelinek said he does see opportunities other than inflation for supermarket operators to increase sales and margins, however. These include maximizing vendor promotional funds, reevaluating private-label assortments, expanding their value offering to other areas, and leveraging loyalty-card data.

In regard to vendor funding, “Retailers need to understand true profitability to understand what the net effect is of a promotional decision,” he said. “In many cases it is much more profitable to look at a decision that drives profitability at point of sale rather than through future bill-back.”

Retailers also have an opportunity to explore their private-label assortments and look at their development costs, weed out duplicated items and consolidate in some areas, Jelinek explained.

Data from loyalty cards also can be increasingly leveraged for targeted marketing efforts, he pointed out.

Hauptman of Willard Bishop also stressed the importance of leveraging loyalty-card data to focus on top shoppers.

“This will become a much more important part of the equation for retailers,” he said. “Even if they might not want to do it solely as a discount vehicle, but also to make better decisions.”

Jelinek also cited five general areas where retailers should look to reduce costs in 2011:

-

Not-for-resale product procurement. This accounts for about 10% of sales at many retailers, and can often be trimmed by 10%, Jelinek said.

-

Working capital/inventory costs. Among the ways he suggests retailers reduce costs in this area is through rationalizing of legacy product assortments, such as those acquired through mergers and acquisitions.

“Look carefully to see where there are duplicate items or duplicate sizes,” he said. “Don't just take out items for the sake of it, but look for those items very specifically.”

In addition, he suggested, many retailers seeking to take out costs might be able to do so with a commissary approach to certain items, particularly in the bakery, meat and deli areas.

-

Pharmacy efficiencies. “Pharmacy tends to be overlooked because it's a small percent of the business, but it can yield a lot of results,” Jelinek said.

Some areas of opportunity include matching hours of operation to hours of demand, optimizing labor costs through the use of pharmacy technicians, and exploring central-fill opportunities in which prescriptions are prepared centrally and either mailed to customers or delivered to stores for pick-up.

-

Reducing freight costs. An analysis of tractor-to-trailer ratios and other asset-utilization parameters can help cut costs, he explained. In addition, delivery schedules should be synchronized to store volumes every quarter, he said.

-

Optimizing store labor. Jelinek said he advocates an approach he calls “return on invested labor,” or ROIL.

“That has to do with looking at the fixed costs, and determining what is the minimum need to operate the stores, and look at that separate from the variable [labor costs],” he said.

“In our experience, we have seen stores not only identify where labor can be appropriated, but the results can yield up to 2% to 3% of revenue increase at the same time, when it's done right.”