Eric Karlson is head of customer strategy, North America, for dunnhumby, helping retailers and brands deliver better experiences through Customer First strategies. The views expressed here are those of the author.

During COVID, the fear of going out in public significantly changed how people shopped in 2020. What happens now to grocery shopping needs as the pandemic fades and people are feeling more comfortable in public? Based on our Retail Preference Index study from 2017 to 2019, most of the variance in financial and emotional performance could be explained by price and quality perceptions. In other words, those banners whose combined price and quality scores where the highest also tended to have the highest financial and emotional performance (H-E-B, Trader Joes, Amazon, Market Basket, Wegman’s, and Walmart). The reverse also holds and those with the lowest price and quality scores tended to have the lowest performance.

During COVID, the fear of going out in public significantly changed how people shopped in 2020. What happens now to grocery shopping needs as the pandemic fades and people are feeling more comfortable in public? Based on our Retail Preference Index study from 2017 to 2019, most of the variance in financial and emotional performance could be explained by price and quality perceptions. In other words, those banners whose combined price and quality scores where the highest also tended to have the highest financial and emotional performance (H-E-B, Trader Joes, Amazon, Market Basket, Wegman’s, and Walmart). The reverse also holds and those with the lowest price and quality scores tended to have the lowest performance.

During the pandemic, however, customers’ needs changed significantly. Speed and safety became the most important drivers while price and quality fell to the bottom. Shoppers were less interested in finding their ideal products at the best price and were instead more interested in purchasing products in a safe environment and were therefore willing to pay extra for that peace of mind. This also meant that purchasing groceries online became a possibility for many who may not have been interested prior to COVID. This additional trial coupled with existing online shoppers helped to double the percent of grocery sales transacting online. This shift in shoppers needs significantly shifted who under- and overperformed in 2020.

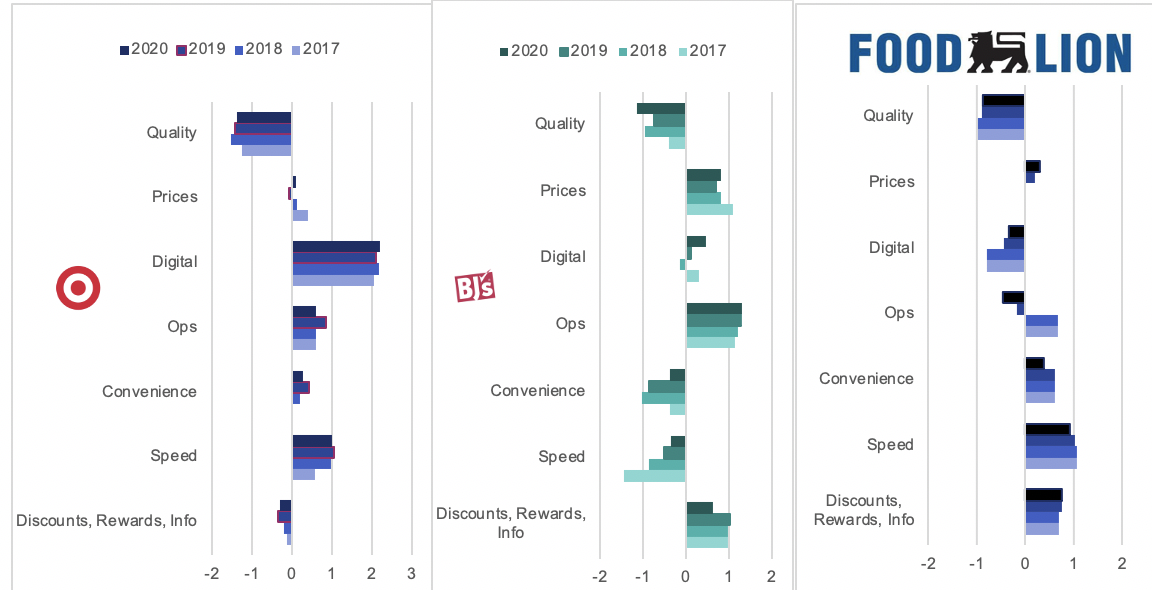

The other interesting question is, did those who outperformed in 2020 do so because they adapted to the new COVID world or was it because they had put in the work before? Essentially, were they already strong in those areas that would be valued by shoppers during COVID? Target, BJ's Wholesale Club and Food Lion all performed significantly better in 2020 versus 2019, and all ranked in the top six out of 60 banners in the COVID Momentum RPI. If their superior performance was due to adaptation, we would expect to see significant improvements in speed, discounts & rewards, and digital in just 2020. If they had already put in the work, we would expect them to be strong in speed, discounts & rewards, and digital before the pandemic. Based on the charts below, the evidence suggests they were already built for Covid as opposed to adapting to the new world.

Our Retail Preference Index study was in the field in October 2020, so shoppers had eight months of COVID shopping to assess the different retailers. Target’s values changed very little but they were strong on speed and digital across the previous four years, which were important trip drivers during 2020. BJ’s did marginally improve in digital during 2020 but their speed pillar has improved every year during the study. In addition, BJ’s in-stock position (operations) also helped. For Food Lion, their speed and discount & reward scores were well established before the pandemic and they had also made improvements in their ecommerce capabilities before COVID. Overall, the scores are largely consistent and we do not see any significant increases in just 2020, and this is consistent across almost all the 60 banners in the study.

What happens if speed and safety become less important in 2021 and 2022? Before COVID, people, on average, shopped at four different grocery retailers per month to find their ideal combination of quality and price. This often included center store commodity items, like paper, household goods, and packaged food, being purchased at mass, club, warehouse or discounters, while the more differentiated perishable products, like meat, produce, prepared food, and dairy, were often purchased at premium and traditional banners. If shoppers return to this pattern, which we expect they will, then price and quality will once again be the key preference drivers.

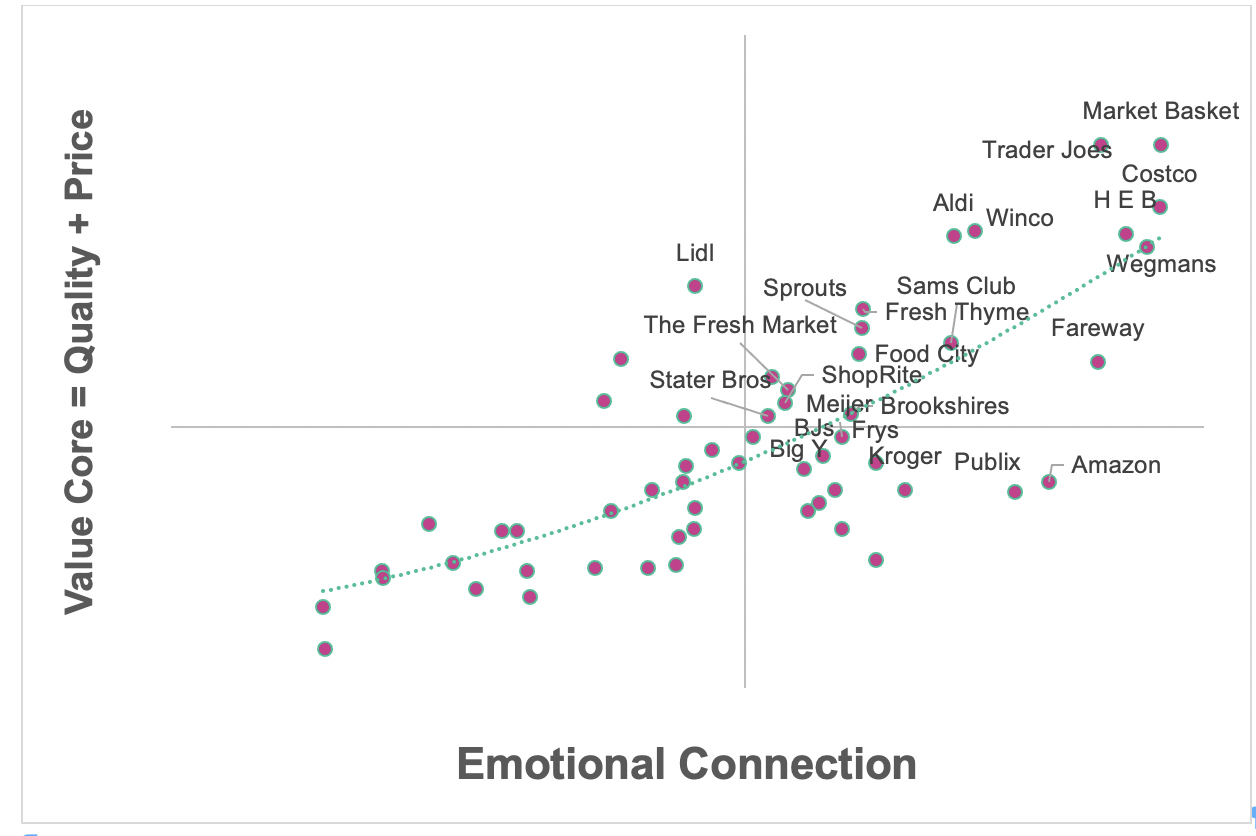

Who wins in a post-COVID world when price and quality come back? We would also bring emotional connection into the analysis. This includes likelihood to recommend, trust and emotional intensity. The stronger this connection, the more likely the retailer will win back customers they lost during COVID and will also help to maintain those that are currently shopping with them. To capture this visually, we added the price and quality scores for the y-axis and placed the emotional connection on the x-axis. Thus, those in the upper righthand corner of the chart below have a strong value core (price + quality) and have a strong emotional connection. The opposite holds for those in the bottom left hand quadrant.

Looking in the upper right-hand quadrant, we see Market Basket, Trader Joe’s, Costco, HEB, Wegmans, Aldi, and Winco. These banners were some of the strongest retailers before COVID, but many stumbled a bit during the pandemic. Some slipped because speed and safety were important and many of these banners are large and perceived to be crowded, so they lost some of these shoppers to the more traditional banners who allowed shoppers to fill-up their baskets relatively quickly and safely even if it cost a bit more. Some, like Wegmans, were hurt by the significant dropoff in prepared food and Market Basket may have been impacted by not having an e-commerce option. In all of these cases, when safety is no longer a concern, we expect to see them rebound, which will likely occur in the back half of 2021 and 2022.

Digging into a few of them, we can see why they slowed during 2020 and why they are well positioned for the future.

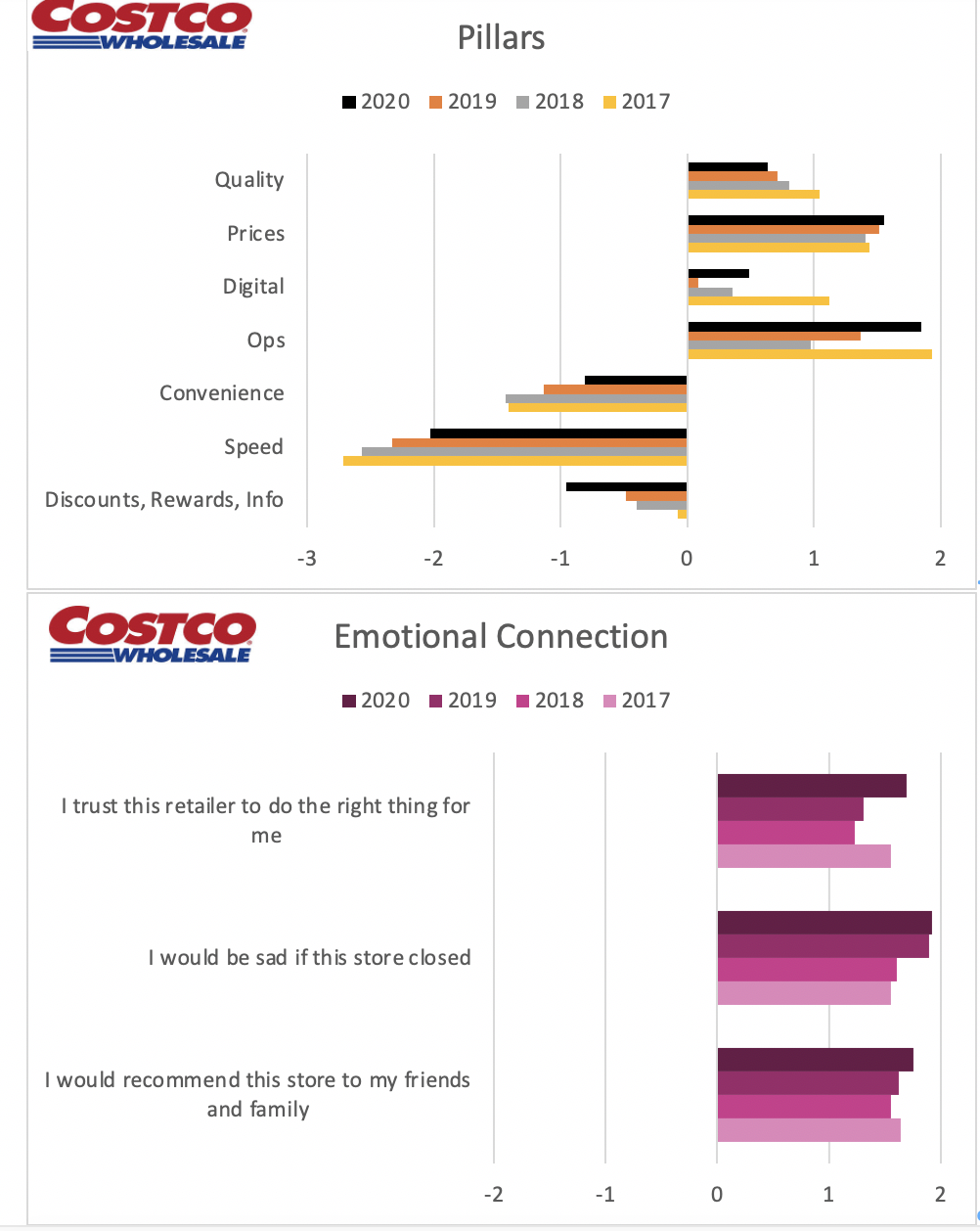

Costco has been a world-class retailer for decades. A $1,000 investment in the 1985 IPO would be worth $130,000 today, which averages out to about 15% per year over 35 years. They are a very large thorn in many traditional banners side because they are one of the few banners to excel at both price and quality which results in a very robust value core. They struggled out of the gate during COVID because of their speed scores and the challenge of doing a full shop in a retailer with less than 5000 skus. They are perceived to be one of the slowest shops in the study, which is not a problem for Costco in non-pandemic years. Moreover, their strong value position translates into one of the strongest emotional connections in the RPI. Costco is already starting to storm back and is a safe bet for the post-Covid market.

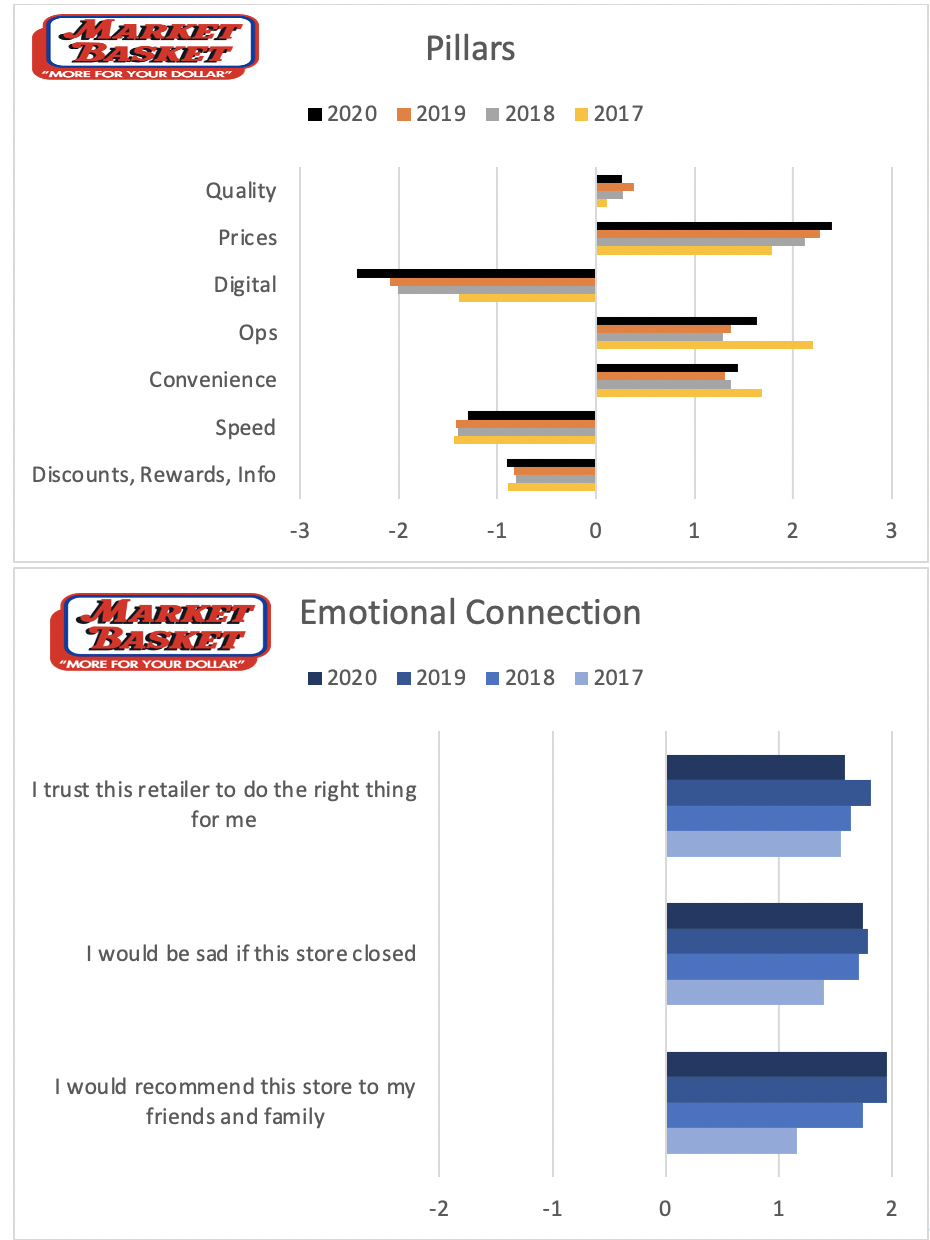

Market Basket is a New England Institution. Their tagline is “More for your Money” and based on their extraordinary price perceptions, they deliver on that promise. This is even more remarkable because they are a traditional banner with less than 100 stores that generate close to $5 billion in sales. To be that strong on price without scale, they have to be the best banner in the U.S. at managing costs. Prior to COVID, they were regularly in the top quartile of our RPI and also regularly in the top five for Consumer Reports ranking. They simply were not built for COVID because they are not known for getting people in-and-out quickly, nor do they spend their hard-earned money on e-commerce. But they do deliver solid quality at very good prices, which has helped to establish one of the strongest emotional connections in the study. As people feel more comfortable returning to the store, Market Basket will re-emerge as a New England market leader.

Wegmans is another strong northeastern retailer that was also not quite built for COVID. Pre-pandemic, Wegmans was consistently in the first quartile of our RPI report. They deliver one of the highest-quality shopping experiences in our study and their prices are near the industry average, thus, they have a very strong value position that translates into a superior emotional connection. However, during COVID their ready-to-eat offering, which was one of the strongest in our study, was significantly impacted. Moreover, their speed pillar was not the strongest and their digital offering was only average. Add all of that up, and Wegmans' relative performance during COVID was not up to historical standards. As the pandemic recedes, Wegmans will regain its prominence as one of the top premium grocery retailers in the U.S.

Over the last year we have been on a roller coaster that has significantly impacted the grocery market. Many perennial pre-COVID power retailers were not at their usual relative strength and many traditional banners were able to steal away some of that share which resulted in some extraordinary years for many traditional banners. We are all interested in understanding how this market shakes out as the pandemic fades. Our data suggests that the back half of 2021 and 2022 will look more like 2019 than 2020 and many of those dominant pre-COVID banners will re-establish themselves in the market.